NumPy¶

NumPy is short for Numerical Python, is the foundational package for scientific computing in Python. It contains among other things:

- a powerful N-dimensional array object

- sophisticated (broadcasting) functions

- tools for integrating C/C++ and Fortran code

- useful linear algebra, Fourier transform, and random number capabilities

Readings¶

SciPy ¶

SciPy is a collection of packages addressing a number of different standard problem domains in scientific computing. Here is a sampling of the packages included:

scipy.integrate: numerical integration routines and differential equation solvers.scipy.linalg: linear algebra routines and matrix decompositions extending beyond those provided innumpy.linalg.scipy.optimize: function optimizers (minimizers) and root finding algorithms.scipy.signal: signal processing tools.scipy.stats: standard continuous and discrete probability distributions (density functions, samplers, continuous distribution functions), various statistical tests, and more descriptive statistics.scipy.cluster: Clustering algorithmsscipy.interpolate: Interpolation and smoothing splinesscipy.ndimage: N-dimensional image processing

Readings¶

pandas¶

pandas provides rich data structures and functions designed to make working with structured data fast, easy, and expressive. pandas rounds up the capabilities of Numpy, Scipy and Matplotlib.

- Primary data structures:

SeriesandDataFrame. - Index objects enabling both simple axis indexing and multi-level / hierarchical axis indexing.

- An integrated group by engine for aggregating and transforming data sets.

- Date range generation (date_range) and custom date offsets enabling the implementation of customized frequencies

- Input/Output tools: loading tabular data from flat files (CSV, delimited, Excel 2003), and saving and loading pandas objects from the fast and efficient PyTables/HDF5 format.

- Memory-efficient “sparse” versions of the standard data structures for storing data that is mostly missing or mostly constant (some fixed value).

- Moving window statistics (rolling mean, rolling standard deviation, etc.)

- Static and moving window linear and panel regression.

Readings¶

Read and write data in Python with stdin and stdout¶

cat ./code/L4/line_count.py

#! /usr/bin/env python3

import sys

count = 0

data = []

for line in sys.stdin:

count += 1

data.append(line)

print("Total ",count, "lines read.") # print goes to sys.stdout

#print(data)

Then launch a terminal and first make your Python script executable. Then send your file to your Python script

chmod +x line_count.py

cat BDE-L3-git.ipynb | ./code/L4/line_count.py

Total 341 lines read.

Read from and write to files directly¶

You can also explicitly read from and write to files directly in your code. Python makes working with files pretty simple.

The first step to working with a text file is to obtain a file object using

open()'r' means read-only

file_for_reading = open('reading_file.txt', 'r')'w' is write -- will destroy the file if it already exists!

file_for_writing = open('writing_file.txt', 'w')'a' is append -- for adding to the end of the file

file_for_appending = open('appending_file.txt', 'a')The second step is do something with the file.

Don't forget to close your files when you're done.

file_for_writing.close()

Note Because it is easy to forget to close your files, you should always use them in a with block, at the end of which they will be closed automatically:

with open(filename,'r') as f:

data = function_that_gets_data_from(f)cat ./code/L4/hash_check.py

#! /usr/bin/env python3

import re

starts_with_hash = 0

# look at each line in the file use a regex to see if it starts with '#' if it does, add 1

# to the count.

with open('~/lectures/code/L3/line_count.py','r') as file:

for line in file:

if re.match("^#",line):

starts_with_hash += 1

print(starts_with_hash)

Read a CSV file¶

If your file has no headers, you can use

csv.reader()incsvmodule to iterate over the rows, each of which will be an appropriately split list.If your file has headers, you can either

- skip the header row (with an initial call to

reader.next()), or - get each row as a

dict(with the headers as keys) by usingcsv.DictReader().

- skip the header row (with an initial call to

#! /usr/bin/python3

data = []

file = open('data/stocks.csv','r')

next(file)

for line in file:

data.append(line)

print(data[0])

AAPL 2015-01-23 112.98

#! /usr/bin/env python3

import csv

data = {'date':[], 'symbol':[], 'closing_price' : []}

with open('data/stocks.csv', 'r') as f:

reader = csv.DictReader(f, delimiter='\t')

for row in reader:

data['date'].append(row["date"])

data['symbol'].append(row["symbol"])

data['closing_price'].append(float(row["closing_price"]))

data.keys()

dict_keys(['date', 'symbol', 'closing_price'])

Alternatively, pandas provides read_csv() function to read csv files.

#! /usr/bin/env python3

import pandas

data2 = pandas.read_csv('data/stocks.csv', delimiter='\t',header=None)

print(len(data2))

print(type(data2))

16556 <class 'pandas.core.frame.DataFrame'>

The pandas I/O API is a set of top level reader functions accessed like read_csv() that generally return a pandas object. These functions includes

read_excel

read_hdf

read_sql

read_json

read_msgpack (experimental)

read_html

read_gbq (experimental)

read_stata

read_sas

read_clipboard

read_pickleSee pandas IO tools for detailed explanation.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.optimize import fmin

import seaborn as sns

# Data available at https://www.kaggle.com/puxama/bostoncsv

# Contains information collected by the U.S Census Service concerning housing in the area of Boston Mass.

boston = pd.read_csv('./data/Boston.csv')

boston.head()

| Unnamed: 0 | crim | zn | indus | chas | nox | rm | age | dis | rad | tax | ptratio | black | lstat | medv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0.00632 | 18.0 | 2.31 | 0 | 0.538 | 6.575 | 65.2 | 4.0900 | 1 | 296 | 15.3 | 396.90 | 4.98 | 24.0 |

| 1 | 2 | 0.02731 | 0.0 | 7.07 | 0 | 0.469 | 6.421 | 78.9 | 4.9671 | 2 | 242 | 17.8 | 396.90 | 9.14 | 21.6 |

| 2 | 3 | 0.02729 | 0.0 | 7.07 | 0 | 0.469 | 7.185 | 61.1 | 4.9671 | 2 | 242 | 17.8 | 392.83 | 4.03 | 34.7 |

| 3 | 4 | 0.03237 | 0.0 | 2.18 | 0 | 0.458 | 6.998 | 45.8 | 6.0622 | 3 | 222 | 18.7 | 394.63 | 2.94 | 33.4 |

| 4 | 5 | 0.06905 | 0.0 | 2.18 | 0 | 0.458 | 7.147 | 54.2 | 6.0622 | 3 | 222 | 18.7 | 396.90 | 5.33 | 36.2 |

- CRIM - per capita crime rate by town

- ZN - proportion of residential land zoned for lots over 25,000 sq.ft.

- INDUS - proportion of non-retail business acres per town.

- CHAS - Charles River dummy variable (1 if tract bounds river; 0 otherwise)

- NOX - nitric oxides concentration (parts per 10 million)

- RM - average number of rooms per dwelling

- AGE - proportion of owner-occupied units built prior to 1940

- DIS - weighted distances to five Boston employment centres

- RAD - index of accessibility to radial highways

- TAX - full-value property-tax rate per $10,000

- PTRATIO - pupil-teacher ratio by town

- B - 1000(Bk - 0.63)^2 where Bk is the proportion of blacks by town

- LSTAT - % lower status of the population: Proportion of population that is lower status = 1/2 (proportion of adults without some high school education and proportion of male workers classified as laborers).

- MEDV - Median value of owner-occupied homes in $1000's

boston.plot(x = 'lstat', y = 'medv', style = 'o', legend=False, ylabel = 'medv')

<AxesSubplot:xlabel='lstat', ylabel='medv'>

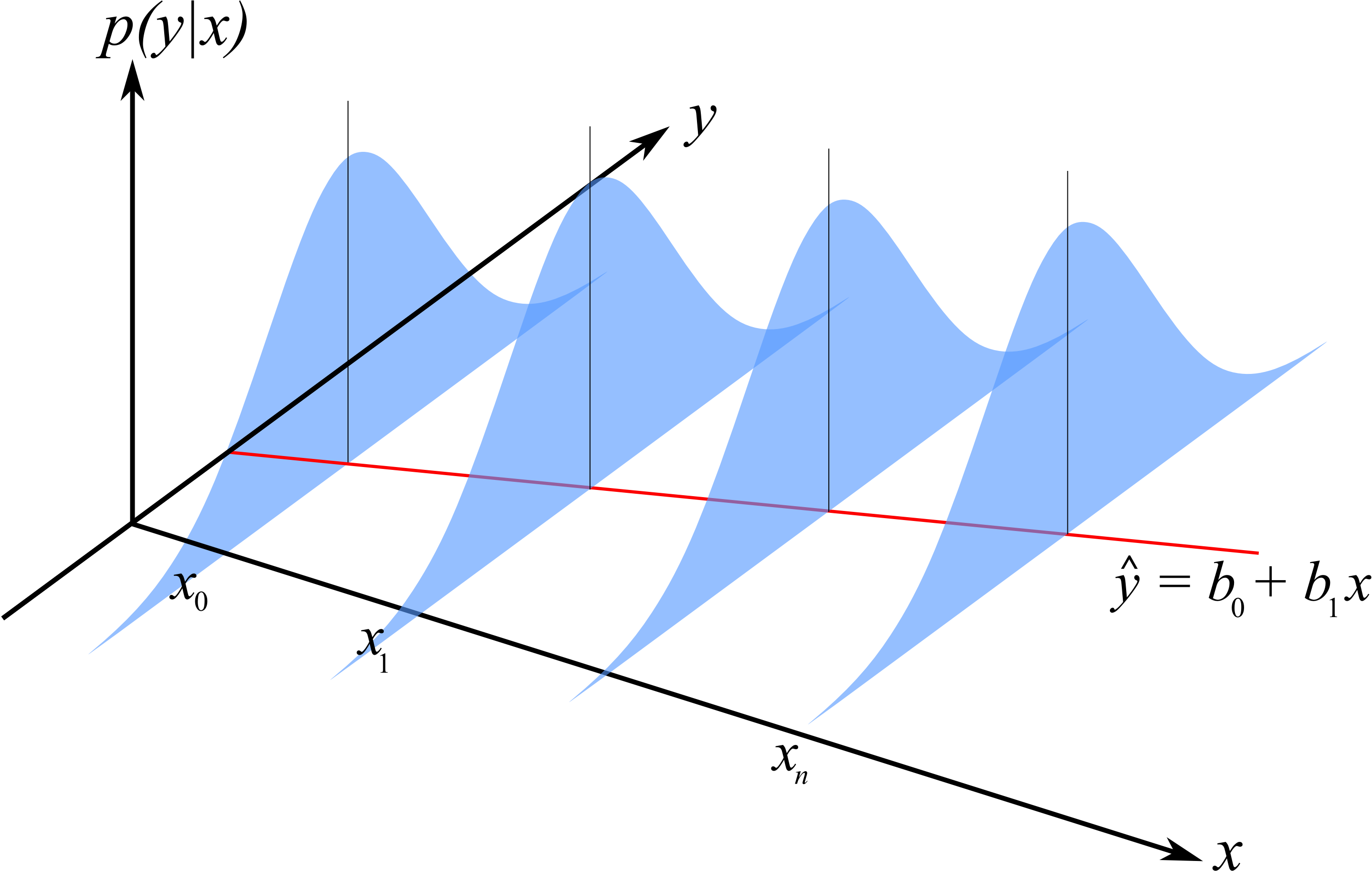

Recall the linear regression model¶

$$Y_i = \beta_0 + \beta_1 x_i + \epsilon_i,~i=1, \cdots, n,~\textrm{where}~\epsilon_i \sim N(0,\sigma^2).$$

We want to minimize

$$f(\beta_0, \beta_1) = \sum\limits_{i=1}^n e_i^2 = \sum\limits_{i=1}^n(y_i - (\beta_0 + \beta_1x_i))^2.$$

Linear regression model¶

What is the distribution of $Y_i$?

sum_of_squares = lambda beta, x, y: np.sum((y - beta[0] - beta[1]*x) ** 2)

sum_of_squares([0,0.7], boston.lstat, boston.medv)

184221.366967

However, we have objective of minimizing the sum of squares, so we can pass this function to one of several optimizers in SciPy.

help(fmin)

Help on function fmin in module scipy.optimize.optimize:

fmin(func, x0, args=(), xtol=0.0001, ftol=0.0001, maxiter=None, maxfun=None, full_output=0, disp=1, retall=0, callback=None, initial_simplex=None)

Minimize a function using the downhill simplex algorithm.

This algorithm only uses function values, not derivatives or second

derivatives.

Parameters

----------

func : callable func(x,*args)

The objective function to be minimized.

x0 : ndarray

Initial guess.

args : tuple, optional

Extra arguments passed to func, i.e., ``f(x,*args)``.

xtol : float, optional

Absolute error in xopt between iterations that is acceptable for

convergence.

ftol : number, optional

Absolute error in func(xopt) between iterations that is acceptable for

convergence.

maxiter : int, optional

Maximum number of iterations to perform.

maxfun : number, optional

Maximum number of function evaluations to make.

full_output : bool, optional

Set to True if fopt and warnflag outputs are desired.

disp : bool, optional

Set to True to print convergence messages.

retall : bool, optional

Set to True to return list of solutions at each iteration.

callback : callable, optional

Called after each iteration, as callback(xk), where xk is the

current parameter vector.

initial_simplex : array_like of shape (N + 1, N), optional

Initial simplex. If given, overrides `x0`.

``initial_simplex[j,:]`` should contain the coordinates of

the jth vertex of the ``N+1`` vertices in the simplex, where

``N`` is the dimension.

Returns

-------

xopt : ndarray

Parameter that minimizes function.

fopt : float

Value of function at minimum: ``fopt = func(xopt)``.

iter : int

Number of iterations performed.

funcalls : int

Number of function calls made.

warnflag : int

1 : Maximum number of function evaluations made.

2 : Maximum number of iterations reached.

allvecs : list

Solution at each iteration.

See also

--------

minimize: Interface to minimization algorithms for multivariate

functions. See the 'Nelder-Mead' `method` in particular.

Notes

-----

Uses a Nelder-Mead simplex algorithm to find the minimum of function of

one or more variables.

This algorithm has a long history of successful use in applications.

But it will usually be slower than an algorithm that uses first or

second derivative information. In practice, it can have poor

performance in high-dimensional problems and is not robust to

minimizing complicated functions. Additionally, there currently is no

complete theory describing when the algorithm will successfully

converge to the minimum, or how fast it will if it does. Both the ftol and

xtol criteria must be met for convergence.

Examples

--------

>>> def f(x):

... return x**2

>>> from scipy import optimize

>>> minimum = optimize.fmin(f, 1)

Optimization terminated successfully.

Current function value: 0.000000

Iterations: 17

Function evaluations: 34

>>> minimum[0]

-8.8817841970012523e-16

References

----------

.. [1] Nelder, J.A. and Mead, R. (1965), "A simplex method for function

minimization", The Computer Journal, 7, pp. 308-313

.. [2] Wright, M.H. (1996), "Direct Search Methods: Once Scorned, Now

Respectable", in Numerical Analysis 1995, Proceedings of the

1995 Dundee Biennial Conference in Numerical Analysis, D.F.

Griffiths and G.A. Watson (Eds.), Addison Wesley Longman,

Harlow, UK, pp. 191-208.

x = boston.lstat

y = boston.medv

b0, b1 = fmin(sum_of_squares, [0,1], (boston.lstat, boston.medv))

b0, b1

Optimization terminated successfully.

Current function value: 19472.381418

Iterations: 82

Function evaluations: 157

(34.55385886222141, -0.9500515380716178)

ax = boston.plot(x='lstat', y='medv', style='o', legend=False, ylabel= 'medv')

ax.plot([0,37], [b0, b0+b1*37])

for xi, yi in zip(x,y):

ax.plot([xi, xi], [yi, b0+b1*xi], 'k:')

Polynomial regession¶

We are not restricted to a straight-line regression model; we can represent a curved relationship between our variables by introducing polynomial terms.

sum_squares_quad = lambda beta, x, y: np.sum((y - beta[0] - beta[1]*x - beta[2]*(x**2)) ** 2)

b0,b1,b2 = fmin(sum_squares_quad, [1,1,-1], args=(x,y))

print('\nintercept: {0:.2}, x: {1:.2}, x2: {2:.2}'.format(b0,b1,b2))

ax = boston.plot(x='lstat', y='medv', style='o', legend=False, ylabel = 'medv')

xvals = np.linspace(0, 37, 100)

ax.plot(xvals, b0 + b1*xvals + b2*(xvals**2))

Optimization terminated successfully.

Current function value: 15347.243159

Iterations: 187

Function evaluations: 342

intercept: 4.3e+01, x: -2.3, x2: 0.044

[<matplotlib.lines.Line2D at 0x7fd5ba6a1e80>]

Generalized linear models¶

Often our data violates one or more of the linear regression assumptions:

- non-linear

- non-normal error distribution

- heteroskedasticity

- this forces us to generalize the regression model in order to account for these characteristics.

As a motivating example, we consider the Olympic medals data.

Linear regression models¶

- Objective: model the expected value of a continuous variable $Y$, as a linear function of the continuous predictor $X$, $E(Y_i) = \beta_0 + \beta_1X_i$.

- Model structure: $Y_i = \beta_0 + \beta_1X_i + e_i$.

- Model assumptions: $Y$ is is normally distributed, errors are normally distributed, $e_i \sim N(0, \sigma^2)$, and independent, and $X$ is fixed, and constant variance $\sigma^2$.

- Parameter estimates and interpretation: $\hat{\beta}_0$ is estimate of $\beta_0$ or the intercept, and $\hat{\beta}_1$ is estimate of the slope, etc. Think about the interpretation of the intercept and the slope.

- Model fit: $R^2$, residual analysis, F-statistic.

- Model selection: From a plethora of possible predictors, which variables to include?

Generalized linear models (GLM)¶

- GLM usually refers to conventional linear regression models for a continuous response variable given continuous and/or categorical predictors.

- The form is $y_i \sim N(x^T_i\beta,\sigma^2)$, where $x_i$ contains known covariates and $\beta$ contains the coefficients to be estimated. These models are usually fit by least squares and weighted least squares.

- $y_i$ is assumed to follow an exponential family distribution with mean $\mu_i$, which is assumed to be some (often nonlinear) function of $x^T_i\beta$.

GLM assumptions¶

- The data $Y_1, Y_2, \cdots, Y_n$ are independently distributed, i.e., cases are independent.

- $Y_i$ does NOT need to be normally distributed, but it typically assumes a distribution from an exponential family (e.g. binomial, Poisson)

- GLM does NOT assume a linear relationship between $Y$ and $X$, but it does assume linear relationship between the transformed response in terms of the link function and the explanatory variables.

- $X$ can be even the power terms or some other nonlinear transformations of the original independent variables.

- Overdispersion (when the observed variance is larger than what the model assumes) maybe present.

- Errors need to be independent but NOT normally distributed.

- It uses MLE rather than OLS.

medals = pd.read_csv('./data/medals.csv')

medals.head()

| medals | population | oecd | log_population | |

|---|---|---|---|---|

| 0 | 1 | 96165 | 0 | 11.473821 |

| 1 | 1 | 281584 | 0 | 12.548186 |

| 2 | 6 | 2589043 | 0 | 14.766799 |

| 3 | 25 | 10952046 | 0 | 16.209037 |

| 4 | 41 | 18348078 | 1 | 16.725035 |

We expect a positive relationship between population and awarded medals, but the data in their raw form are clearly not amenable to linear regression.

medals.plot(x='population', y='medals', kind='scatter')

<AxesSubplot:xlabel='population', ylabel='medals'>

Part of the issue is the scale of the variables. For example, countries' populations span several orders of magnitude. We can correct this by using the logarithm of population, which we have already calculated.

medals.plot(x='log_population', y='medals', kind='scatter')

<AxesSubplot:xlabel='log_population', ylabel='medals'>

This is an improvement, but the relationship is still not adequately modeled by least-squares regression.

This is due to the fact that the response data are counts. As a result, they tend to have characteristic properties.

- discrete

- positive

- variance grows with mean

To account for this, we can do two things:

- model the medal count on the log scale;

- assume Poisson, rather than normal.

Poisson regression¶

- So, we will model the logarithm of the expected value as a linear function of our predictors:

$$y_i \sim \text{Poisson}(\lambda_i)$$ $$\log(\lambda_i) = \eta_i = \beta_0 + \beta_1x_{i,1} + \cdots + \beta_1x_{i,q},$$

Log link function forces positive mean.

Poisson log likelihood:

$$\log L = \sum_{i=1}^n -\exp(x_i^T\beta) + y_i (x_i^T \beta)- \log(y_i!)$$

- As we have already done, we just need to code the kernel of this likelihood, and optimize!

# Poisson negative log-likelhood

poisson_loglike = lambda beta, X, y: -(-np.exp(X.dot(beta)) + y*X.dot(beta)).sum()

b1, b0 = fmin(poisson_loglike, [0,1], args=(medals[['log_population']].assign(intercept=1).values,

medals.medals.values))

b0, b1

Optimization terminated successfully.

Current function value: -1381.299433

Iterations: 68

Function evaluations: 131

(-5.297302917060439, 0.44873025169011005)

ax = medals.plot(x='log_population', y='medals', kind='scatter')

xvals = np.arange(12, 22)

ax.plot(xvals, np.exp(b0 + b1*xvals), 'r--')

[<matplotlib.lines.Line2D at 0x7fd5b8d999a0>]

More on modeling¶

Statsmodelsfor advanced modeling.Scikit-learnfor statistical learning.